Lets face it, no one is born with money management skills, and all of us have made our share of mistakes with trying to manage our finances. We often experience frustration, disappointment, shame, anger, guilt, and jealousy.

Managing your finances is a skill that must be learned and it is never too late to start. I am going to share with you the ways that I have learned to manage my finances, and I hope that they help you as much as they have helped me.

The main thing that you have to remember is that “It’s not how much you make, but what you do with what you’ve got.” It is all about getting the most from what you already have.

I have some simple “STEPS” that you can follow that are guaranteed to help you create a budget that works.

Shortcut menu:

Step 1: Set Your Goals

Identify what is important to you. What do you want to do? You may want to:

-

buy a house

-

travel

-

pay for your kid’s education

-

start a business

-

pay off credit cards

-

build up your savings account

-

save to get a business loan

-

save up for a moderate down payment

These are just a few of many ideas to help you get started. What you choose is your goal and only your goal. You have the power to choose what is important to you and design your goals accordingly. Then you need to think about how much you need to save and for how long. How will you accomplish this? …all great questions to think about when setting a budget.

It is important to be realistic when setting your goals. You can increase savings later down the road, but you want to start out by planning successfully. Ideally, you wan to plan your short term, intermediate term, and long term goals.

Short term goals should be those goals that you want to achieve within the next year.

Intermediate goals are those goals that you want to achieve within the next 5 years.

Long term goals are those goals that you want to achieve within the next 10 or more years.

For Each Goal you want to:

-

Set your objective

-

Estimate the Cost of the goal

-

Set a Target Date

-

Calculate Monthly Funds Needed

-

Figure out How Much you will be putting aside per pay period

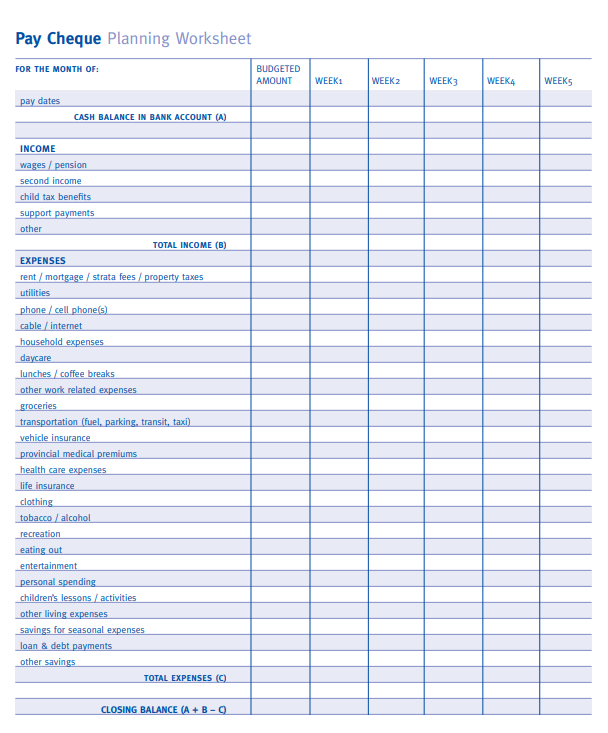

Step 2: Identify Income & Expenses

Now that you have set your goals for your income, you need to determine where your income comes from and where it is going. I have supplied a sample budget worksheet to help you.

Start by making a list of all your household income sources and the amounts. Include everything: wages after taxes, commissions, self–employment income, pensions, and other regular income.

Next, it is time to calculate your expenses. This may be a little hard to do because we may know where our income comes from, but we may not be as certain where it is going. Include EVERYTHING you may spend your money on, like bills, groceries, transportation, savings, debt payments, insurance premiums, etc. They are all expenses.

Similarly, it is important to record your spending for two or three months. The purpose of tracking your spending is to find out where all the money is going.

You may forget to record some items, but it is very important to try to remember to record your spending because it is an imperative part of identifying your expenses. Do not try to track “how you think you should be spending”. These are not accurate reflections of your spending. This is the time to learn what you are currently doing with your money.

Step 3: Separate Your Wants From Your Needs

While tracking your spending, you may find out that some of your income is spent on things you really don’t need. Unplanned spending is also known as Impulse Spending… purchasing things that you may or may not need, or spending more on an item than you’d planned.

Good money management skills start with separating your needs from your wants. If you are not sure if an item is a need or a want, try going without it for a period of time. If you truly can’t live without it during that period, it is a need. Also, just because one item costs more than the same item, it does not mean that the more expensive item is better for you. We do NOT want to keep up with the Jones’, because we do not know their situation.

Step 4: Design Your Budget

Some may think that the word Budget means “limitations”. I am here to tell you that it is actually the opposite. Your budget is your spending plan, allowing you to live within your means and avoiding stressful and difficult financial troubles. It also gives you the freedom to make choices, and helps you to reach those goals that you have set.

It is very important at this stage that your expenses do not exceed your income. This is the opportunity to make some choices based on what you learned when you tracked your spending and when you separated your needs from your wants.

Review your Budget worksheet making sure that your total spending is not more than your total income. Also, ask yourself, will this budget allow me to reach my goals? You may have to cut back on spending in some areas of your budget compared to how you have spent in the past. Your money could be needed somewhere else in your budget. You may also want to add any extra money to your savings.

If you are experiencing financial difficulty, savings may be the furthest thing from your mind, however, even during this time, it is so important that you plan to have money for the unexpected. Setting money aside for savings is the difference between having a budget that works and one that doesn’t. Not only does it protect you from financial disaster, it also helps you to meet your financial goals.

If you have a healthy savings available to pay for living costs and seasonal expenses if an emergency arises, you do not need to rely on credit.

Emergency savings covers your basic living costs in case there are changes in your income. For example, in the event of a job loss, it typically takes 3 months to get back on track with either a new source of income or outside assistance. During this time, you still need money for rent, groceries and other essentials; this is what your emergency savings is for. Jump start your savings account (if you can afford it) with your income tax refund, or unexpected bonus.

In addition to emergency savings, it is necessary to have general savings which you can use to meet your financial goals and ensure your sound financial future. I like to refer to this a “paying yourself first”. If you are able, open a savings account and have your bank automatically transfer funds into this account without you seeing the money first. The common saying “out of sight, out of mind” is a good thing to remember regarding your savings account.

There is no magic number that tells you what you should be saving each month. It depends on your income level, your debt load, your life stage, if you are employed, unemployed or retired as well as your financial goals.

At first you may find it difficult to set savings aside. If you have outstanding debts to pay or you aren’t in the habit of saving, it’s important to get started. Save a small amount from each pay check at first and increase the amount as you are able to. You’ll be amazed at how quickly your savings can add up once you just get started!

Step 5: Action Plan

Goals are set, income and expenses identified, you have determined how much you are going to save for expenses, and you have reviewed your wants and needs. Now it’s time to put your plan into action!

I like to use a pay check plan to match your spending patterns to your income schedule. If you are paid every two weeks, then use a two-week schedule; if monthly, then a monthly schedule.

In the budget column, record what you need to spend. Money that you set aside in a savings account is an expense that you deduct from your income.

-

Note your pay dates across the top.

-

If you have money in your bank account that you need for this month’s expenses, note that as income for this month as well. Don’t forget to subtract any checks you have written that have not cleared your account yet.

-

Record your net pay checks amount for each pay date. List any other income you receive during the month in the week you will receive it.

-

Decide when the expenses from your budget column will be paid. This will depend on your pay dates. Start with expenses that are due on specific dates, like bills and insurance premiums. Try to balance the expenses evenly throughout the month.

-

Total your income from each pay period and if there is any left over, add it to your savings account. If you are short, re-examine your expenses to see what you are able to reduce or evaluate if you are able to increase your income.

For those with Irregular Incomes that do not have a steady job with a steady pay check, or those who are seasonal workers, self employed, or work on commission, it may be even harder to manage your income. It does not mean that you can’t create a budget, but it does mean that you need to plan in more detail. Part of the planning process must include a separate savings account for income tax payments at the end of the year. And if you are self-employed, you must take deliberate steps to separate your personal and business finances.

If you have had irregular income for a few years, one strategy is to calculate the average net income you’ve had per year for at least 3 years, divide by 12 and use that amount to build your current budget. If this amount is not enough to meet your expenses, you must consider how you can increase your income or decrease your expenses to make your budget balance.

Another way to build a budget if you have irregular income is to set up a holding account. All of your income is deposited into the holding account. You pay yourself a monthly amount based on what you have identified you can afford and what will allow you to meet your obligations. During months of higher income, the holding account will have a larger balance. During the leaner months, the holding account balance will decrease. However, the amount you pay yourself does not vary from month to month.

Step 6: Managing Your Seasonal Expenses

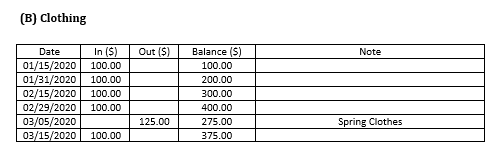

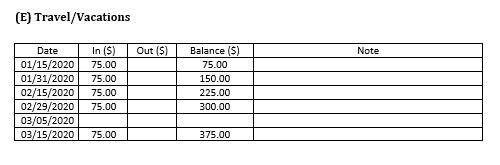

Now that you have created a workable budget and have planned your pay checks and funds, the last step is to plan your savings money so that you are able to track and manage your seasonal expenses more precisely.

Set up a binder with one page for each expense item listed on your Budget Worksheet. The first page is what is actually in your savings account (A). List the date and how much you deposit or withdraw each time. The subsequent pages are for the items you will need money for when the time comes, like car repairs, gifts, clothing, etc.

For example, you deposit $300 to your savings account twice a month and record this on the first page of your binder (A). Then, based on your budget, you record the amount you need for your expenses on each of the next 4 pages as follows:

*** B + C + D + E has to equal A at all times.

When an expense occurs and you spend money from your seasonal savings account, for example, $20 on a gift for your child, record on the first page (A) what you withdrew $20. Then on the “gift” page (D), subtract $20 from the amount listed there and note the reason.

The important thing to remember is that the total of your seasonal expense pages (b+c+d+e) must total what you actually have in your savings account.

Planning how to spend your saved money, just as you do your pay checks, will allow you to have the money you need when you need it.

Step 7: Looking Ahead

Any good plan must involve monitoring, periodic review, and occasional re-evaluation. A spending plan is no different. Circumstances may change, mistakes can be made and your needs will vary at different times in your life.

When you first build your spending plan, you are going to need more time to monitor it to ensure that it is based on realistic information. It will take a month to start falling into place.

During the second month, you will work out some of the kinks and the routine will start to become part of your daily thinking. It should now start to fall into place more easily.

By the third month, your spending plan should be up and running. Congratulations, you have taken control of your finances! However, if it isn’t working yet, ask yourself a few questions:

-

Did I calculate my income correctly?

-

Are my expense figures accurate?

-

Is everything accounted for?

-

Is my plan based on actual numbers or what I hope I can earn or spend?

-

Did I give it a fair chance?

-

Do I need professional advice?

For the first year, you will need to review your plan monthly. If it is working, during the second year you can review it every 3 – 4 months. After that, you will need to review it annually. However, if there are any major changes in your financial life, you will need to re-evaluate your plan and possibly change it. Some major changes might include increased transportation or housing costs or a loss or increase of income. Similarly, large purchases or expenses may mean that you will need to cut back somewhere else so that everything fits again.

As you become more in the habit of managing your money effectively, your plan will feel natural and develop into a part of how you do things in your household. Some of the steps may blend together at times or you may add a step or two to make it easier for yourself.

Life happens; give yourself permission to make changes that benefit you and your family. Having a plan with a solid foundation will allow you to come out ahead, rather than in debt.

A Note About Credit

Yes, it is true that Credit can afford us opportunities that may not be available to us otherwise. Most people who purchase their first home need a mortgage. Same for a Car purchase. However, in order to avoid burdensome and expensive debt, you need to plan how you will use credit responsibly within what your budget allows. Some things to keep in mind to protect your credit rating as well as your financial plan:

-

Only apply for credit that you need. One, maybe two credit cards, with very reasonable limits based on your income, are all you should need. Pay them off in full every month.

-

Keep all credit card balances well below the limits on all of your cards at all times.

-

Keep credit limits reasonable – if you used or charged them all to the limit, you should be able to pay the full balance off within a year and leave it paid off.

-

Pay more than the minimum payment due each month on a credit card and work on bringing the balance owing down. Limit your use of the card until it is paid in full.

I hope this information helps you get your finances and financial freedom back in line. It has helped me and I KNOW it will help you. Just take your time. There is no rush. You GOT this!

James

Leave a Reply

Your email is safe with us.